A Study of the Watch Auction Market in 2022

By Russell Sheldrake

The auction market has always been the public face of the vintage and pre-owned watch world. Their yearly seasons, with headline lots and colourful catalogues, grab the attention of collectors around the world. As 2021 saw the rest of the world begin to slowly recover from the pandemic, the auction houses managed to achieve record numbers, nearly doubling the figures from 2020.

All this growth is set against the backdrop of booming online sales, with a near constant stream of virtual offerings from the big houses falling in direct competition with newer, online-only platforms. Given the remarkable nature of the auction market today, and how it has rapidly evolved over the past couple of years, we wanted to uncover what had prompted this rapid expansion, as well as where its possible limitations might lie. To do so, we have gathered thoughts from across the industry, speaking with leading auctioneers, ex-auction-house employees and veterans of the bidding scene to gain as many perspectives as possible.

All of this is in aid of trying to predict the future of the market, to understand how it might evolve and what we might come to expect from this ever-changing area of our industry. Whether it’s the physical locations of the auctions themselves, the watches going into them, or the demographic of those placing bids, the recent changes look set to continue in the coming years.

A Brief History of Watch Auctions

Officially speaking, watch auctions started with Antiquorum and Osvaldo Patrizzi. They were the first auction house to dedicate not just a department but the core of their business to selling clocks and watches. While wristwatches weren’t their sole focus when they opened in 1974 – the market was nowhere near mature enough for this yet – it wouldn’t take long for Patrizzi’s enterprising spirit to shine through. “Everything you see in watch auctions today was introduced by Osvaldo and Antiquorum,” explains William Massena. A veteran of the auction scene, Massena was, at one point, COO of Antiquorum, and today runs the collaborative brand Massena LAB. “From thematic auctions to condition reports and live online bidding, everything started at Antiquorum,” he adds.

A collection of early auction catalogues from Galerie d’Horlogerie Ancienne, which later became Antiquorum, courtesy of Christie's.

Once Patrizzi had shown that there was a market in this space, the traditional auction houses – namely Christie’s and Sotheby’s, which had been around since the 18th century – opened their own dedicated departments. Massena is keen to point out that this did not mean that they suddenly became the forces we know them to be today. Rather than instantly building relationships with key collectors, the majority of their lots came from estate sales. Some of the more famous examples were the Jackie O and Andy Warhol sales, both of which housed a significant number of watches.

However, while we are focusing on watches, it is important to remember that timepieces were, and still are, a fraction of an auction house’s business in total. “When you can sell one painting for the same as an entire watch auction, what do you think you’re going to focus on?” Massena points out. Christie’s recently released their total sales figures for its Luxury departments, which consist of jewellery, handbags, wine and spirits, and watches. In 2021, these departments totalled $980 million in sales, including private sales – yet watches only made up $205 million of that total. If watches only accounted for roughly 20 percent of these combined departments in a record-breaking year, it puts into perspective how relatively small the market is.

Osvaldo Patrizzi, founder of Antiquorum, courtesy of Europa Star.

These large estate sales brought a healthy amount of attention to the watch departments of Christie’s and Sotheby’s, and allowed them to steadily grow over the next few years. However, despite this, the dealers that were growing in number throughout Europe and Asia would mainly be seen at Antiquorum auctions. “It could be a very intimidating place for collectors, surrounded by dealers,” says Massena. “If you didn’t know who they were, [or were not] part of their club, it was a very tough place to be.” This tightly knit circle ruled the auction scene for many years, sourcing much of their stock to sell to the growing community of collectors.

A small group was also able to control the market to a certain extent. “Everyone knew everyone,” Wulf Schuetz tells us. Owner of vintage dealer Rare & Fine, Schuetz has been around the auction scene for a long time, starting when Patek Philippe were looking to build up their museum collection in the very early days. “And back then, nearly every bidder was in the room as well.” Further down, we’ll get onto how the location of bidders – and the medium through which bids are placed – has changed things.

-

Early catalogues from Christie's, Sotheby's, and Dr. Crott Auctioneers, courtesy of Wulf Schuetz

-

-

-

While Christie’s and Sotheby’s established themselves and their departments in the watch space, smaller, regional players started to rise in significance as well. Houses such as Dr. Crott Auctioneers in Aachen; Ineichen Auctioneers in Zurich; Artcurial in Paris; and even Bonhams in London, to a certain extent, were beginning to make their presence felt. Yet their small steps were overshadowed by the giant leaps that Antiquorum were making. In 2001, Patrizzi was able to sell off a major collection owned by the chairman of HSBC, Lord Sandberg, which helped to massively push their overall sales figures. Alongside these increasingly impressive results, Patrizzi was also establishing the tradition of academic research in modern horology. Writing countless books, as well as providing detailed descriptions and condition reports on each lot, he started to prove that there was an audience out there that not only wanted to buy a watch, but wanted to learn about it as well.

We can thank Patrizzi for one of the big innovations in this space: the thematic sale. The very first came in 1989, in the shape of The Art of Patek Philippe. This sale was a real milestone in the history of watch collecting, as it outlined a structure that would prove massively popular up to the current day. It also showed just how passionate the collecting base for watches – and timepieces of all sorts – was in the late 1980s.

The first ever thematic sale for watches, organised by Patrizzi and Antiquorum, The Art of Patek Philippe in 1989, courtesy of Habsburg Feldman.

Moving into the mid-2000s, Antiquorum began to wane and, in its place, Sotheby’s and Christie’s took a commanding position over the industry. With Daryn Schnipper leading the charge at Sotheby’s, and the young forces of Aurel Bacs and John Reardon developing impressively at Christie’s, it seemed that these two houses were engaged in a back-and-forth race to hold dominance over the market. It could be argued that at the beginning, Sotheby’s was slightly ahead, especially after their sale of the Henry Graves Super Complication in 1999 – often regarded as the first true headline lot. However, by the time they got it back in 2014, with Bacs buying it as a proxy bidder for $24 million, Christie’s seemed to be overtaking. They managed to reach more than $123 million in annual sales, while Sotheby’s fell just short of reaching $100 million.

While we began by singing the praises of Antiquorum and Patrizzi, any keen market observer will know that today they no longer enjoy a position at the very top. There were mistakes made that led to a slow decline that can be traced from the mid-2000s onwards – from their failed launch of live online bidding to a lawsuit that ended operations entirely in New York. It could be said that Patrizzi was too ahead of his time, attempting to push the market in ways that it either wasn’t ready for, or where the technology wasn’t developed enough to sustain it.

Daryn Schnipper, who is currently the chairman of the International Watch Division at Sotheby's.

After he left Antiquorum, Patrizzi founded another auction house called Patrizzi & Co, a short-lived venture that suffered from the same issues that had plagued him at Antiquorum. So little has been heard of Patrizzi in the last few years that many in the watch-collecting space today have no idea who is, despite everything he has done for the industry.

Antiquorum had its best results in 2006, the year before Patrizzi left, with sales close to $74 million. To put that into perspective, Phillips recently reached that total in one sale at their Geneva Watch Auction: XIV, totalling $74.5 million. In the last 15 years, Antiquorum have never contested for the highest value in sales, with Christie’s and later Phillips remaining dominant. This highlights auction houses’ “key man risk” – something highlighted to us by Schuetz. We’ll come back to that later.

While the profiles of Reardon and Schnipper rose after Patrizzi’s departure, one person seemed to have a clearer vision and command more attention when wielding a gavel than any other. That was, of course, Aurel Bacs. Having previously worked at Sotheby’s and Phillips (known as Phillips de Pury at the time), he really rose to prominence at Christie’s. Here, he honed his vision of how a watch auction should be run and began to capitalise on the potential that was in this space.

Aurel Bacs after leaving Phillips de Pury and when he was with Christie's, courtesy of the FHH Journal.

Bacs established himself at Christie’s, proving that he could command an auction room better than most. “If you’re not passionate about watches, you’ll never be able to sell them,” Bacs tells us. “And I think I’m more passionate about them than anyone else out there.” This passion has helped him to not only gain the highest prices for watches over the years, but secure consignments for some of the very rarest pieces.

The line of succession from Patrizzi to Bacs is fairly clear. Patrizzi’s willingness to innovate and push boundaries, paired with his natural showmanship and flair with the gavel, made him a favourite among dealers and collectors. Today you can see all the same attributes in Bacs. When at Christie’s, he was put on the team that would develop their online capabilities – and their software was later sold all around the world. While Bacs will freely admit he doesn’t have an intimate knowledge of how these things work, he can bring the auctioneer’s perspective to them, ensuring that the end user’s experience matches their expectations.

“What Bacs did when he started at Phillips was monumental,” says Nicholas Biebuyck, TAG Heuer’s Heritage Director and a regular on the auction scene. “The vision that he installed there was like nothing we had seen before, although in some ways it was an extension of what he started when he worked with them back when they were Phillips de Pury. I really do think we will talk about the watch auction business pre- and post-Aurel at Phillips.”

The catalogue cover of the Phillips Geneva Watch Auction: XIV from November 2021, courtesy of Phillips.

Today, the three major houses still operating in watch auctions appear to have found their own niches and are doing everything they can to capitalise on them. Phillips is leading the way in terms of live auctions, focusing all their energy on highly curated physical sales that achieve much higher prices per lot, a tactic driven by Bacs’ “instincts”. A great example of this is a quick breakdown of the value of watches sold at the Geneva Watch Auction: XIV in November, where 248 lots were sold – 112 of which went for more than CHF 100,000. Meanwhile, Christie’s and Sotheby’s seem to be charting similar courses of continuing to run live auctions, but massively strengthening their online-only offerings. Sotheby’s seems to lean most heavily into the digital space, holding 38 online-only sales last year, compared to Christie’s 23. Ever since their sale to Patrick Drahi, a French-Israeli telecoms billionaire, Sotheby’s have increasingly invested in their digital strategy, with initiatives such as their NFT-dedicated platform showing just how serious they are when it comes to online sales.

With this context in mind, it’s worth considering the real strengths and weaknesses in today’s market. Which areas are ripe for growth, and where are we likely to see some shrinkage or slowing down? It can be hard to predict what might happen next without mapping out those areas that are likely primed for change in 2022.

The Strengths of Watch Auctions

The big three houses – Phillips, Christie’s, and Sotheby’s – carry an immense amount of power when it comes to consignees deciding on where to sell their watch. Their history, public exposure and large offices around the globe make them an attractive option, as it gives them the credibility and a sense of trustworthiness that is hard to come by in today’s digital age. Despite the watch departments only making up a small part of these organisations, if you are looking to shed multiple assets – maybe some old furniture, a painting and a few watches – the auction houses are the best and only places to go to.

A selection of watches from the upcoming Christie's Watches Online: The Dubai Edit auction, courtesy of Christie's.

We can see from the 2021 results that the watch-auction business did better than ever, with a larger increase in sales figures than ever before, nearly doubling the numbers we saw in 2020. Between Phillips, Christie’s, Sotheby’s and Antiquorum, 2020 sales totalled just shy of $347 million, excluding private and charity sales. This number jumped last year, to reach more than $607 million. There are plenty of reasons for this unprecedented growth, from a ballooning watch market in general to a remarkable increase in auction houses offering online sales. Many of our commentators highlighted virtual sales as the biggest opportunity for growth in the auction business.

Sotheby’s and Christie’s are looking to shorten the delays that are inherently built into the auction business. For example, big auction houses’ traditional yearly cycles seem to be broken thanks to near continuous online-only offerings. This means that there is always something to bid on, satisfying the year-round appetite for buying and selling.

Being able to shift much higher volumes at much lower prices means that the work of an auctioneer looked quite different in 2021 than it did just two or three years before. Sam Hines, the soon-to-be-outgoing Worldwide Head of Watches at Sotheby’s, agrees. “Live auctions can take four months, [from] start to finish, but with a watch we are putting online, it could be up on the site within a week of it arriving and gone soon after that.” This quick turnaround is a massive incentive for many buyers; they have started to see the benefits of the online dealer model, where a watch can be turned around much more quickly than it can be within an auction house. This marks a shift in mentality from inside the houses, too. “It used to be the case that if there was a watch we didn’t want to put into a live auction, it would go online,” Hines tells us.

The live auction of Paul Newman’s watch in 2017 at Phillips, courtesy of Phillips.

You can see the effect this has had on the value of watches sold at both Christie’s and Sotheby’s, as watches with higher values are harder to sell through this method – although Christie’s did manage to sell a Patek Philippe reference 5002P-001 for $1.6 million. Meanwhile, Phillips seem to be tackling the online space in a different way. To take the most extreme example, the blue-dial, Tiffany-signed Patek Philippe 5711 broke the record for an online sale at auction. Despite not selling to the winning bidder, it did hammer online for $6.5 million. This piece also broke the record for the number of online bidders registered for a specific lot, at 378. Instead of spreading out their online audience, Phillips are concentrating them on specific pieces at specific auctions, where they are likely to make the most impact.

Of course, the pandemic has had a big impact on this segment of the market. With a lack of travel opportunities, those who would have otherwise attended in person were forced to stay in their home country and compete from their laptop or phones. As we all got used to telecommuting and Zoom meetings, this naturally extended to other areas of our lives. While the watch world is normally slow to evolve, as Biebyuck put it, “in Sotheby’s, especially, we’ve seen four years of transformation in about four months”. Schuetz points out that “online sales have limitless scale opportunities” when compared to physical auctions. This is why there is such potential seen in platforms such as Loupe This, which are pushing the model of online-only auctions.

The online platforms of Sotheby's and Loupe This.

The sense of theatre created around live sales is another area of strength that we have seen for a long time in the auction business, and holds true to this day. As Schuetz says, “It’s exciting being in the room and competing against other bidders.” This sentiment was echoed by Eric Ku, a veteran collector and dealer, and recently a co-founder of online auction site Loupe This. “Auctions are really exciting – nothing can replicate the excitement of being in an auction room and seeing these world records being set one after the other,” he notes. Perhaps the master of capturing this excitement is Bacs – “You cannot fabricate emotion,” he says. It’s hard to replicate the feeling that is generated when two bidders are going head-to-head on a lot that has been talked about for the last month. While some people have questioned the continued need for live, in-person auctions, Bacs puts it very simply: “Where do you see rock concerts in the future?”

It feels like the future of physical watch auctions is safe in the hands of Bacs and his team. As an example, those who went to the winter auctions in New York last December felt far more positive about it than seemed possible in the depths of the pandemic. However, it was exciting to see not just the numbers of people in attendance, but also those who amassed online to bid. The technology to allow this has been in place for quite some time, but it took the pandemic for bidders to truly adopt it and for auction houses to make the most of it.

Aurel Bacs at work, courtesy of Thomas de Cruz Media.

According to the data released by Phillips, 92 per cent of their lots last year had online bids placed on them, with 52 percent of the lots being sold to those online bidders. It’s clear that this is something that the houses’ clients want to do more of, even if there is a sentimental push to get back into the auction room. Patrick Y, a moderator and editor at Watch Pro Site, points out that one big advantage of this system is that it’s more convenient for those located in different time zones. The auctions that take place in Geneva are often timed so that collectors in Tokyo and New York can take part in sociable hours, making these a true representation of global tastes and pricing. Meanwhile, those that happen in New York or Hong Kong can often exclude one half of the world.

As the lines between digital and physical auctions have become more blurred, the traditional definition of what makes a classical auction timepiece has become similarly muddied. The market used to be dominated by vintage Patek Philippe and similar historical pieces, whereas if you look at most of the top lots at the big three auction houses last year, you will notice a massive influx of strikingly modern, independent, or current production models. This diversification was brought into real focus when Phillips decided to headline early and significant pieces by both F.P. Journe and Philippe Dufour in one sale. These collections possibly made an even bigger splash than when Sotheby’s managed to sell an incredibly fresh Patek Philippe pink gold reference 1518.

The Patek Philippe pink gold ref. 1518 sold by Phillips alongside the Patek Philippe 5002P-001 sold by Christie's.

This excitement around newer watches seems to also be drawing in bigger and younger crowds, as the media coverage becomes a little easier to understand for those who perhaps aren’t well versed in the annals of Patek Philippe history. The media coverage surrounding the auction scene certainly seems to have picked up its pace over the last couple of years. Previously, it was limited to the odd forum post or report on Hodinkee, whereas we are now seeing record-breaking sales reaching mainstream sites and big lot announcements being shared worldwide.

While we will go on to investigate areas that could be improved in the watch auction space, from the numbers that have been published for last year, it is clear that buying a timepiece using the auction format is more popular than ever. Bacs partly puts this down to the entire watch space growing in popularity. “When I started, there were no clients in China, but now we see Asia as one of the biggest markets,” he says. “Globally, the pool of people capable of buying a watch has grown.” This theory is confirmed by Hines, who says, “When I started, we probably had around 300 bidders. Now we are at about 3,000.” In all the online sales that Sotheby’s held last year, Hines believes that between 40 and 50 percent of bidders were new to the company.

A live auction in Christie's Hong Kong, courtesy of Christie's.

Younger bidders are another demographic that has been wielding more power in recent years. Not only has cryptocurrency made many freshly minted millionaires out of Millennials and Gen Z, but those who inherit generational wealth or who have built up and sold their first company before turning 30 are looking at watches as a show and store of wealth. However, Shawn Mehta, owner of Watch4moi and a young collector himself, believes that these new bidders are doing so in equally new ways. “The most important thing is probably the privacy aspect,” he says. He believes that younger bidders often prefer to bid online so that they remain discrete and, due to their age, this will be far more natural to them than those who still remember the introduction of the dial-up modem. Many of those we spoke to recognise that this group is driving an increase in prices as well. “I just don’t know when it will cool off – prices are just going up every week,” comments Hines. Whether this is strictly a strength or not depends on your point of view, and is a debate aired among collectors on an almost daily basis.

However, if we didn’t have auctions, it would be a lot harder to judge a true market price for many of these watches. Schuetz believes that “the collecting market needs public auctions”. While they may only represent a fraction of the second-hand watch industry – believed to total $18 billion in sales in 2019 – they will often show what price at least two people are willing to pay for a watch, setting the value for similar pieces around the world. As Schuetz told us further up, this was less true when the market was smaller, but it is now, thanks to the global reach and the amount of serious money entering the market today.

John Reardon, founder of Collectability and the previous International Head of Watches at Christie's and Alexandre Ghotbi of Phillips Geneva.

Auction houses offer fantastic standardisation when it comes to the buyer’s perspective, as Ku points out. “The listings look better, there is a professional copywriter, photos are consistent,” he says. “You also get an unbiased professional opinion of your piece – we have a scoring system for our watches. That’s something that you don’t get when people list their own watches on something like eBay.”

Alongside this standardisation, Remy Julia, Director at Christie’s Dubai and Head of Watches Middle East, believes that the big auction houses offer institutionalised security. “We have a structure, with exhibition areas, showrooms, and specialists who are available to appraise the watches, but also to advise the buyers,” he says. “[This creates] a premium service, comfort, and unequalled security.”

The Risks of the Auction Market

Despite the incredible growth we have seen over the last 12 months, there are still a few flaws and weaknesses in the auction market, and it still has certain limitations in 2022 – including the ways the houses structure their fees and the long periods consignees can often wait to be paid.

Unpaid lots are a growing concern, and not just for the auction houses. As we saw recently, the star watch of the New York Phillips auction, the very first Patek Philippe 5711 Tiffany blue dial, went unpaid after hammering at $6.5 million. Luckily, there was a fairly vocal and visual under-bidder in the auction room, Zach Lu, who is not only known to Phillips – their website suggests he is currently still a consultant for them – but also Patek Philippe, as he claims that he has known Thierry Stern since the age of 15.

The infamous Patek Philippe 5711 Tiffany blue dial, courtesy of Phillips.

It is extremely rare for such a transaction, as detailed in the Hodinkee article, to be made public. However, with the level of exposure that the watch and auction had (Lu was even photographed at the sale mid-bid), it seems impossible for the news not to reach a wider audience. This was especially true in this case, as the under-bidder shared an unboxing video, featuring Paul Boutros, with his Instagram followers. Despite the multiple checks that are made in advance of a client being allowed to bid, based on conversations that we’ve had with those in the auction world, there appear to be more occasions than one might think that clients are either unable – or unwilling – to pay the price they committed to.

These unpaid lots don’t just present a risk to the auction house – they represent an issue of trust across the entire market. One of the biggest advantages of a public sale is that it offers a fair market value that is visible and accessible to all. Yet unpaid lots are never made public, and neither is the price that is eventually paid for them – assuming they are bought at all. If no one is willing to reach the reserve, they could either go back to the consignee or end up in a future auction. With such a high-value lot as the Tiffany 5711 going unpaid, it suggests that this problem may occasionally affect some of the most important market values.

Lu bidding on the Tiffany 5711, courtesy of Hodinkee.

Auction houses will likely never expose these unsold lots, or the prices that they eventually sell for – an issue that Mehta speaks to us at length about. “Auction houses need radical transparency,” he comments. While everyone uses the publicly listed results of auction houses to determine market values, including Mehta himself, it is hard to put 100 percent faith in their results when it’s clear a certain number will never be paid for at that price. Today, with a massive influx of online and telephone bidders, it’s almost impossible to know who you’re bidding against – something that Schuetz is keen to point out to us, as he notes how much things had changed in the last 20 years.

This issue has been, in part, created by the old system used by auction houses. Bidders are given 30 days to pay for a lot, so many things can happen to stop a bank transfer from going through. Companies such as Loupe This work around this by taking an automatic payment of up to $10,000 as soon as bidding closes, ensuring that anyone placing a bid can pay at least this amount while the auction is taking place.

Platforms like Loupe This also offer both bidders and consignees a far simpler and more streamlined fee system. The premium charges by the big houses have been increasing steadily over the years and recently went up from 25 to 26 per cent across most of them. “The fee structure of traditional auctions is pretty high,” says Ku. “It’s beneficial when you’re selling a multi-million-dollar watch, but not necessarily when you’re selling a lower-priced item. We think that our business model, with a significantly lower fee structure, is more interesting for certain types of watches.”

Telephone bidders at a live auction, courtesy of Sotheby's.

Loupe This only take 10 percent of a buyer’s fee, and sellers pay a $500 upfront flat charge to submit the watch. While these fees all sound impressive, it’s perhaps more striking that all this information is easily found on their website. If you were to peruse the website of several auction houses, there is no number given for how much a seller is charged for listing their watch with them – a lack of transparency that goes back to the point Mehta made earlier. Patrick Y sums this up quite nicely: “It takes a long time, they take a large percentage and, as a consigner, you’re not always going to net the most at an auction house.”

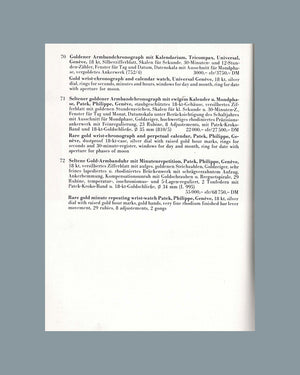

Some people feel that there is also room for improvement in the way auction houses deal with lots being removed from sale. There have been very few instances where these removals have made a big splash and a significant number of people have noticed. Often, the only way to spot the lots that disappear is if they have already printed the catalogue and the watch never comes up during the auction. Without external pressure, or direct questioning from a client, there will never be any explanation as to why a watch was removed. While this can be to help protect the original consignee, it often appears to be protecting the auction house and their own reputation. However, as the market grows and the number of people paying close attention to auctions increases, it will become harder and harder for the house to remove lots without notice or explanation.

Steve McQueen and the controversial Rolex Submariner, courtesy of Hodinkee.

Perhaps the most famous example of this was back in 2018, when Phillips were forced to withdraw a Steve McQueen Rolex Submariner from their Racing Pulse December sale. This was a dispute between the McQueen estate and the story that Phillips initially published. It is extremely rare for a timepiece of such high importance to be pulled, particularly after the extensive amount of PR that goes into such big auctions and their star lots (it is far more common for smaller lots to lose their spot in a catalogue). When this happens, however, a public announcement is very rarely made. Mehta likens this to the auction houses “drawing in sand”.

According to Patrick, in the minds of the auction houses, buyers often play second fiddle to sellers – something he has personally experienced. “Auction houses generally favour the seller as they are much harder to recruit than the buyers,” he says. “As a buyer, you’re really coming in on the bottom rung of the house.” This can mean that the average watch buyer will have far less sway than those who regularly partake in art sales. We have been told that this disparity becomes clear when a buyer tries to contact the auction house. Only so many resources can be allocated to handle them and, in many locations, the watch department is limited to just a few people.

A number of observers note that auction houses have been known to depend too much on one person – a phenomenon known as “key man risk”. Patrizzi leaving Antiquorum was a key example: while his near-celebrity status within the industry was a real draw for both bidders and sellers, once he left, the house never seemed to regain its market share.

A George Daniels Anniversary Watch and a Patek Philippe Ref. 1436 at the preview for the Phillips Geneva Watch Auction in 2019.

It is possible to make a comparison to Aurel Bacs and when he left Christie’s at the end of 2013. The house ended that year with more than £130 million in total sales, but it would take them until 2021, and a huge boost in online sales, to surpass that number again. It could be argued that they saw this sustained drop in figures thanks to Bacs leaving the house and just a year later establishing himself at Phillips. This begs the question: what would happen at Phillips, should Bacs decide to leave? He has managed to build a strong team around him since joining, with the likes of Alex Ghotbi in Geneva, Paul Boutros in America and Thomas Perazzi in Hong Kong all carving their own niches and establishing themselves separately from Bacs. Of course, this is all speculative, and there are far more complex forces at work on the auction market than the output of one person.

What Does the Future Hold For Auctions?

This is where things can get a little tricky. There is clearly a high demand for auctions moving forward, as we can see from the incredibly strong numbers the major auction houses have posted in the last 12 months. However, the alternatives seem to be getting better and better every year. Whether it is the rise of Loupe This, or a stronger pre-owned structure on eBay, it’s clear that the growth opportunity in online auctions is huge. As Mehta put it, “eBay is the dormant giant”.

The draw of auction houses still holds sway over the market, whether it’s through their large, theatrical live sales, their continual online offerings, or their more discreet private sales that they facilitate. The market is clearly strong, yet whenever the topic comes up, there will always be those who point out the downsides. There are inherent limitations to selling or buying through auction and, now that the market has grown to a certain size, some people are looking to capitalise on these weaknesses. Many of those who we spoke to believed that if the auction houses are not able to keep pace with the rise of online-first platforms, then they will eventually suffer.

Eric Ku, the founder of Loupe This.

Remy Julia sees a big division coming to the market. “The biggest trend, I think, is that there is going to be a split in the auction world between collector watches and luxury watches,” he says. This split seems indicative of a growing market, as more buyers enter the market we are going to see more variation in not only what they are looking for, but also their motivations for buying. According to Julia, of the online sales that they held last year from Dubai, 48 percent of clients (both bidders and sellers) were new to Christie’s. This incredibly high percentage illustrates just how far-reaching these online sales can now be – far beyond the traditional watch market or passionate collectors.

Alongside this growing market, it is reaching younger buyers and sellers than ever before. “With the growth of the digital world and online sales, there are now collectors all over the world, and they are getting younger and younger,” says Julia. In the past two to three years, this has meant a growing interest in newer watches and an insatiable appetite for change. This constant drive to find the “next thing” seems to be led by the more youthful segment of the market.

Bacs at a Phillips auction in 2019, courtesy of Phillips.

However, as Bacs points out, the theatre of a live auction will always draw a crowd. He likens online auctions to the online weddings of the pandemic, where the virtual version could never compare to the real thing. Many of those we spoke to believe that live auctions are in safe hands with the likes of Bacs and his team at Phillips. Their formula seems to not only be the most popular, but the most effective at bringing in and selling the top lots. However, what this will mean for the other watch departments remains to be seen. As Schuetz points out, “There is limitless growth potential online.” It’s just a question of whether or not the auction houses have the capability to truly capture it.

We would like to thank all who helped inform this article including, Wulf Schuetz, William Massena, Aurel Bacs, Sam Hines, Remy Julia, Nicholas Biebuyck, Eric Ku, Shawn Mehta, and Patrick Y.